/cloudfront-us-east-2.images.arcpublishing.com/reuters/6NZOUEPAP5K2JGDADAU4SJDHKQ.jpg "Banks beware, Amazon and Walmart are cracking the code for finance")

LONDON, Sept 17 (Reuters) – Everyone can be a banker these days, you just will need the appropriate code, Benefit Group.

International brand names from Mercedes and Amazon (AMZN.O) to IKEA and Walmart (WMT.N) are chopping out the conventional economical middleman and plugging in program from tech startups to offer you buyers anything from banking and credit rating to insurance coverage.

For proven financial institutions, the warning signs are flashing.

So-known as embedded finance – a extravagant term for firms integrating software program to supply monetary solutions – suggests Amazon can permit prospects “buy now shell out later on” when they look at out and Mercedes drivers can get their vehicles to pay back for their gas.

To be sure, financial institutions are however guiding most of the transactions but investors and analysts say the possibility for standard lenders is that they will get pushed more away from the entrance close of the finance chain.

And that implies they’ll be more absent from the mountains of knowledge other folks are hoovering up about the choices and behaviours of their consumers – information that could be important in offering them an edge in excess of financial institutions in economical providers.

“Embedded fiscal expert services usually takes the cross-sell idea to new heights. It truly is predicated on a deep computer software-based mostly ongoing details marriage with the consumer and organization,” stated Matt Harris, a associate at trader Bain Funds Ventures.

“That is why this revolution is so essential,” he explained. “It implies that all the great chance is going to go to these embedded corporations that know so a great deal about their buyers and what is left over will go to banking companies and insurance coverage firms.”

Exactly where DO YOU WANT TO Engage in?

For now, quite a few parts of embedded finance are scarcely denting the dominance of financial institutions and even even though some upstarts have licences to supply regulated providers these types of as lending, they lack the scale and deep funding swimming pools of the major banks.

But if monetary technology companies, or fintechs, can match their accomplishment in grabbing a chunk of digital payments from banking institutions – and boosting their valuations in the approach – lenders may well have to reply, analysts say.

Stripe, for instance, the payments platform powering numerous sites with customers like Amazon and Alphabet’s (GOOGL.O) Google, was valued at $95 billion in March.

Accenture believed in 2019 that new entrants to the payments marketplace had amassed 8{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of revenues globally – and that share has risen in excess of the earlier calendar year as the pandemic boosted digital payments and strike regular payments, Alan McIntyre, senior banking sector director at Accenture, mentioned.

Now the aim is turning to lending, as effectively as comprehensive off-the-shelf electronic loan providers with a variety of goods corporations can select and choose to embed in their procedures.

“The huge the greater part of purchaser centric organizations will be able to start financial solutions that will allow them to considerably boost their buyer experience,” claimed Luca Bocchio, lover at venture capital business Accel.

“That is why we experience energized about this space.”

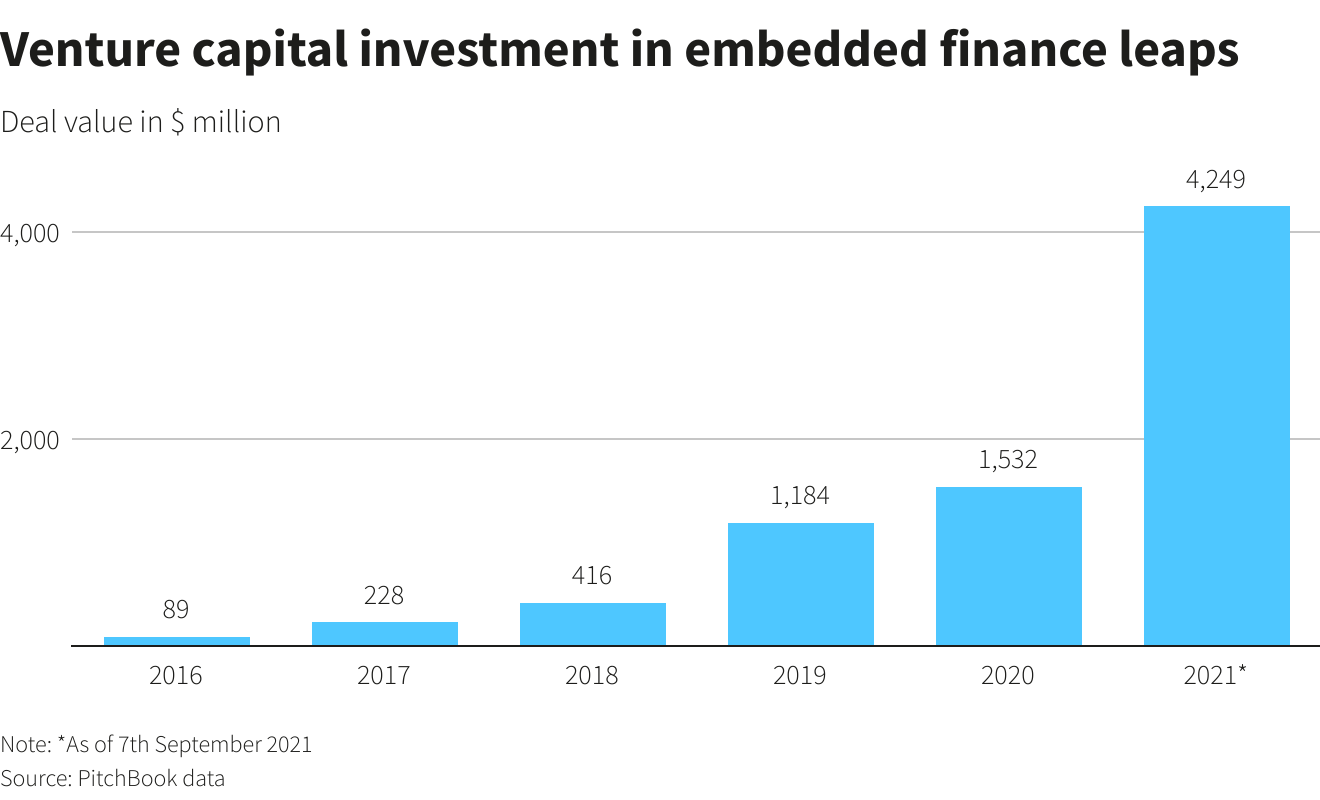

So far this yr, traders have poured $4.25 billion into embedded finance startups, virtually three situations the quantity in 2020, information offered to Reuters by PitchBook demonstrates.

Primary the way is Swedish acquire now pay back later (BNPL) business Klarna which elevated $1.9 billion.

DriveWealth, which sells technology allowing for companies to offer you fractional share trading, captivated $459 million whilst traders put $229 million into Solarisbank, a accredited German electronic financial institution which offers an array of banking companies application.

Shares in Affirm (AFRM.O), in the meantime, surged previous thirty day period when it teamed up with Amazon to provide BNPL products whilst rival U.S. fintech Square (SQ.N) mentioned last thirty day period it was obtaining Australian BNPL firm Afterpay (APT.AX) for $29 billion.

Square is now really worth $113 billion, additional than Europe’s most precious lender, HSBC (HSBA.L), on $105 billion.

“Massive financial institutions and insurers will get rid of out if they will not act swiftly and operate out exactly where to enjoy in this industry,” claimed Simon Torrance, founder of Embedded Finance & Super Application Tactics.

YOU Have to have A Financial loan!

Numerous other retailers have announced strategies this calendar year to broaden in money products and services.

Walmart launched a fintech startup with financial commitment firm Ribbit Money in January to acquire economical goods for its personnel and buyers when IKEA took a minority stake in BNPL firm Jifiti final month.

Automakers such as Volkswagen’s (VOWG_p.DE) Audi and Tata’s (TAMO.NS) Jaguar Land Rover have experimented with embedding payment technological innovation in their autos to take the trouble out of having to pay, in addition to Daimler’s (DAIGn.DE) Mercedes.

“Consumers assume providers, which include money solutions, to be immediately integrated at the position of intake, and to be hassle-free, digital, and quickly accessible,” mentioned Roland Folz, chief executive of Solarisbank which gives banking companies to a lot more than 50 firms such as Samsung.

It’s not just conclude buyers being targeted by embedded finance startups. Companies themselves are remaining tapped on the shoulder as their digital facts is crunched by fintechs these kinds of as Canada’s Shopify (Shop.TO).

It gives software package for retailers and its Shopify Cash division also delivers income innovations, based mostly on an analysis of far more than 70 million data points throughout its platform.

“No service provider comes to us and suggests, I would like a personal loan. We go to retailers and say, we believe it’s time for funding for you,” explained Kaz Nejatian, vice president, product, service provider providers at Shopify.

“We don’t request for business plans, we never ask for tax statements, we never question for cash flow statements, and we really don’t inquire for personal assures. Not due to the fact we are benevolent but due to the fact we think those are undesirable alerts into the odds of achievement on the online,” he explained.

A Shopify spokesperson claimed funding goes from $200 to $2 million. It has presented $2.3 billion in cumulative funds advances and is valued at $184 billion, well previously mentioned Royal Bank of Canada (RY.TO), the country’s most important traditional lender.

Linked Long term?

Shopify’s lending company is, however, however dwarfed by the large financial institutions. JPMorgan Chase & Co (JPM.N), for instance, experienced a buyer and neighborhood personal loan e-book worth $435 billion at the stop of June.

Key developments into finance by organizations from other sectors could also be constrained by regulators.

Officers from the Financial institution for Global Settlements, a consortium of central banks and monetary regulators, warned watchdogs past month to get to grips with the growing influence of technologies corporations in finance. read through a lot more

Bain’s Harris stated monetary regulators were getting the tactic that mainly because they do not know how to regulate tech firms they are insisting there’s a bank at the rear of each and every transaction – but that did not mean financial institutions would avert fintechs encroaching.

“They are proper that the banks will always have a purpose but it is not a extremely remunerative part and it entails incredibly little ownership of the customer,” he stated.

Forrester analyst Jacob Morgan said banks had to make your mind up exactly where they want to be in the finance chain.

“Can they afford to combat for purchaser primacy, or do they truly see a much more worthwhile route to industry to grow to be the rails that other individuals run on prime of?” he stated. “Some financial institutions will decide on to do each.”

And some are currently fighting again.

Citigroup (C.N) has teamed up with Google on financial institution accounts, Goldman Sachs (GS.N) is delivering credit cards for Apple (AAPL.O) and JPMorgan is getting 75{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of Volkswagen’s payments organization and strategies to broaden to other industries. study extra 06:00:00

“Connectivity in between distinct devices is the potential,” explained Shahrokh Moinian, head of wholesale payments, EMEA, at JPMorgan. “We want to be the chief.”

Reporting by Anna Irrera and Iain Withers Editing by Rachel Armstrong and David Clarke

Our Expectations: The Thomson Reuters Belief Rules.

Visit : https://benefitgroupltd.com/