/cloudfront-us-east-2.images.arcpublishing.com/reuters/HJ5EF7J3BJM7FKGUJOMA5MHOUY.jpg "Analysis: Banks that helped GE, others bulk up now profit from break-ups")

Nov 16 (Reuters) – Some of the Wall Road banking companies that helped Typical Electric Co (GE.N), Toshiba Corp (6502.T) and Johnson & Johnson (JNJ.N) turn into massive conglomerates through acquisitions more than the a long time are now profiting from their break-ups, a Reuters investigation showed.

The a few firms, which in recent days introduced programs to spin off divisions, doled out hundreds of thousands and thousands of bucks in expenses to banking institutions, which include Goldman Sachs Group Inc (GS.N), JPMorgan Chase & Co (JPM.N) and UBS Team AG (UBSG.S), to recommend them on acquisitions above the many years. Now, the similar banks are finding compensated to undo the results of these discounts.

Spokespeople for Goldman Sachs, JPMorgan and UBS did not reply to requests for remark.

Even though it is really not unheard of for an expenditure bank to suggest a firm on a spin-off just after beforehand performing on the firm’s acquisitions, the spate of substantial-profile spin-offs by companies in modern days shines new light on the practice.

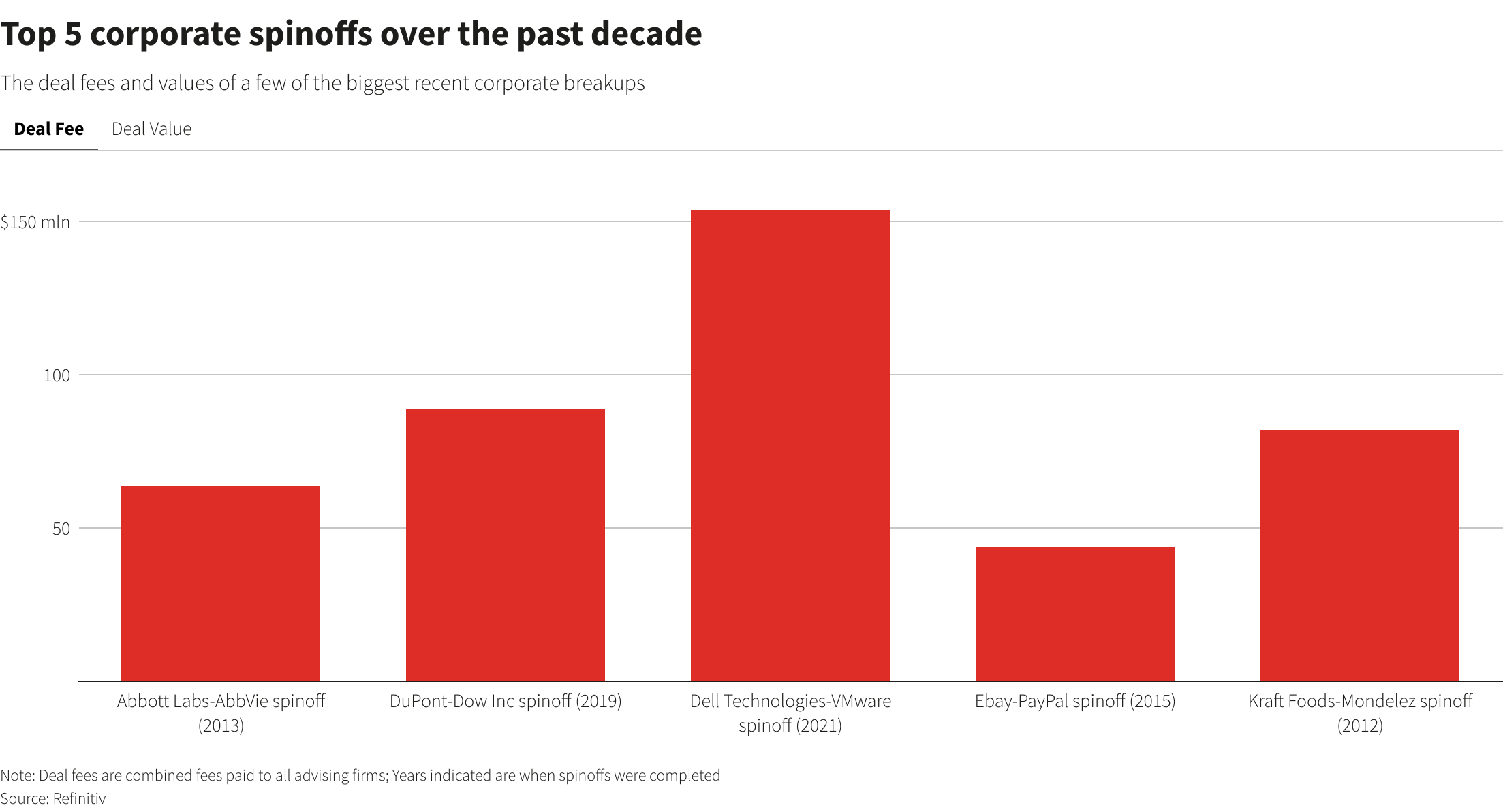

Banking institutions have so far attained around $1 billion on spin-offs globally so significantly this yr, nearly 2 times what they gained in 2020, in accordance to Refinitiv.

Traders in all those providers are not confident comparable riches. Shares of organizations that interact in acquisitions or divestments have experienced a mixed observe history, usually underperforming friends in the last two several years, according to Refinitiv.

Erik Gordon, a professor of law and company at the University of Michigan, stated banks do not commonly split any principles when performing on these discounts due to the fact they are carrying out their clients’ needs. But he pointed out that this did not absolve banking institutions of the obligation to advise versus a deal they perspective as not in a company’s long-phrase curiosity.

“If the bankers ought to have criticism, it is for not pushing again towards a CEO who pushes a lousy offer,” Gordon reported.

In the circumstance of GE, Goldman Sachs was one particular of the financial institutions, together with Evercore Inc (EVR.N), PJT Partners Inc (PJT.N) and Lender of The usa Corp (BAC.N), that stand to collect tens of hundreds of thousands of dollars from advising on the company’s split-up, in accordance to estimates from M&A lawyers and bankers.

Goldman Sachs had beforehand gathered approximately $400 million in charges advising the organization on acquisitions, divestitures and spin-offs due to the fact 2000, generating it GE’s major adviser based mostly on M&A fees collected, according to Refinitiv.

JPMorgan, which recommended J&J on its prepared crack-up, experienced previously created $206 million in expenses considering the fact that 2000 advising it on deals, according to Refinitiv. UBS, which labored on Toshiba’s crack-up, experienced collected $12 million in costs, the Refinitiv details showed.

Industrywide, Goldman Sachs has earned the most in costs from advising on corporate split-ups thus significantly in 2021, followed by JPMorgan and Lazard Ltd (LAZ.N), in accordance to Dealogic.

Corporate crack-ups are on the increase amid a expanding consensus on Wall Street that corporations complete finest only if they are focused on adjacent business enterprise parts, as well as rising pressure from activist hedge resources pushing them in that route.

Some 42 spin-offs collectively worth about $200 billion have been introduced globally so far this calendar year, up from 38 spin-offs really worth roughly $90 billion in 2020, in accordance to Dealogic. Investment decision banking companies have collected additional than $4.5 billion considering that 2011 advising on spin-off offers globally, the Dealogic knowledge shows.

For an interactive graphic, click on this connection: https://tmsnrt.rs/3cgKJ9M

Independent Suggestions

Expense bankers generally argue that providers did not automatically get it improper when they embarked on bargains they later on reversed, since some mixtures do not make perception for good.

Alterations in a company’s technological and aggressive landscape or in the angle of its shareholders can thrust it to alter study course.

For example, GE shareholders were initially supportive of its empire-making acquisitions in companies as numerous as health care, credit history playing cards and amusement in the 1990s, viewing them as diversifying its earnings stream. When some of these enterprises commenced to underperform and GE’s valuation endured, buyers shed religion in the firm’s means to operate disparate firms.

Bankers also argue that most companies want to spend bankers for delivering deals relatively than information on whether they have to have to do a deal in the 1st location. This results in incentives for bankers to consider to clinch a transaction somewhat than persuade a greater outcome for their consumer that could not include a offer.

But it also features ammunition to Wall Road critics who argue that companies can not depend on banking companies for impartial information on no matter if they should pursue a deal.

“Organizations really should produce valuations in home and with aid from impartial 3rd-bash advisers, no matter if or not they also employ an expenditure bank,” mentioned Nuno Fernandes, professor of finance at IESE Organization School.

Reporting by Anirban Sen in Bengaluru and David French in New York Editing by Greg Roumeliotis and Stephen Coates

Our Expectations: The Thomson Reuters Rely on Rules.