ThitareeSarmkasat/iStock via Getty Images

Investors concerned about inflation and rising interest rates should consider BlackRock bank loan closed-end funds for income.

Bottom line

- Hot inflation readings and expectations for Fed rate increases may cause investors to rethink their portfolio allocations

- Bank loans can offer attractive yields and may benefit from these trends, particularly relative to “fixed” income assets

- Investors should consider BlackRock’s bank loan closed-end funds for efficient access to bank loans with the potential for monthly income and opportunities to buy the funds at a discount to net asset value

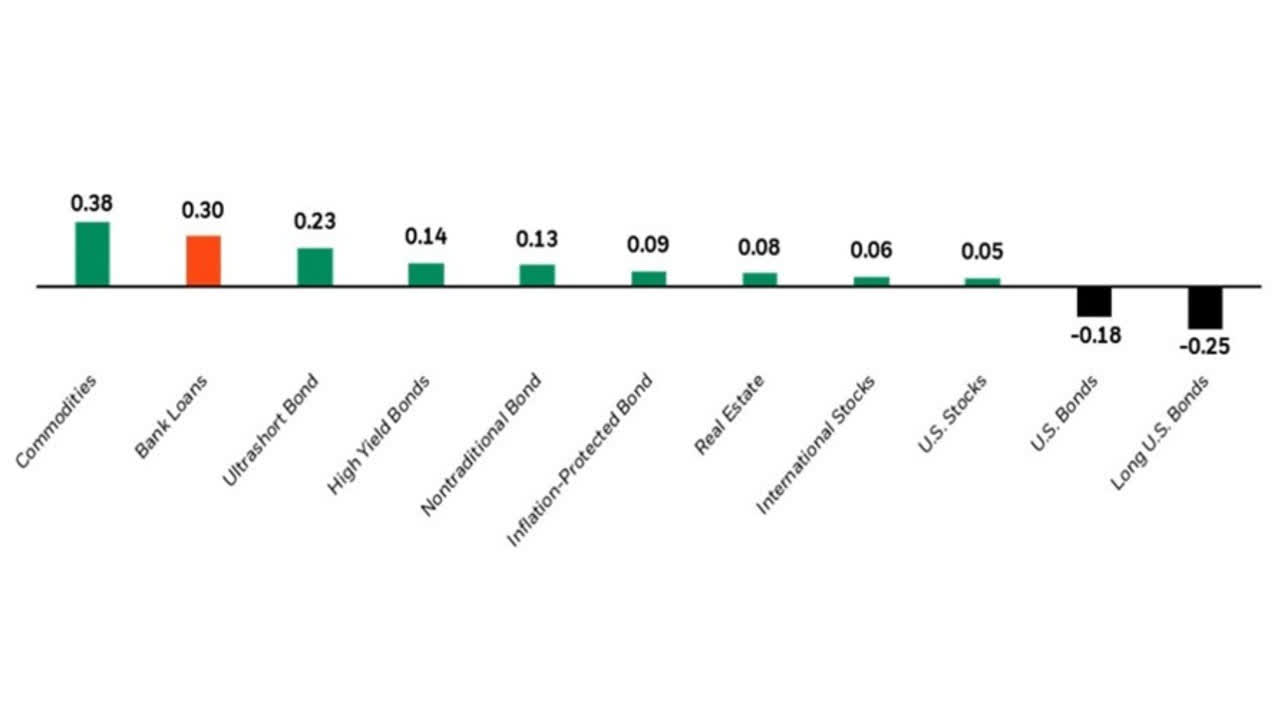

The start of 2022 has been marred with market volatility across asset classes. Elevated inflation readings and the prospect for structurally higher interest rates are at the forefront of investors’ minds. This environment may lead some investors to rethink their longer duration fixed income exposure. Many investors are turning to bank loans, also known as floating rate loans, which are debt instruments whose coupon is linked to a short-term interest rate like LIBOR or SOFR. Given the floating rate nature of the asset, adding bank loans to your portfolio can lower duration and increase potential income as the Fed looks to continue raising short-term interest rates to combat the recent surge in inflation. Historically, bank loans have performed well in rising interest rate environments and have had a positive correlation to inflation (Exhibit 1).

BlackRock Floating Rate Income Strategies Fund (FRA), BlackRock Floating Rate Income Trust (BGT), and BlackRock Debt Strategies Fund (DSU) (together the “BlackRock Bank Loan CEFs” or the “Funds”) provide actively managed and diversified exposure to the bank loan sector and may be appropriate for investors seeking income and the potential for capital appreciation. Given certain structural advantages and the potential to fund at a discount, we believe BlackRock Bank Loan CEFs may be an attractive investment opportunity today.

Exhibit 1: Bank Loans have had a positive correlation to inflation

Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only.

You cannot invest directly in any index. Source: Commodities are represented by the S&P GSCI TR Index, Bank loans by the S&P/LSTA Leveraged Loan TR Index, Ultrashort bonds by the Morningstar US Fund Ultrashort Bond category, High yield bonds by the Bloomberg US High Yield 2{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} Issuer TR Index, Nontraditional bonds by the Morningstar US Fund Nontraditional bond category, Inflation-protected bonds by the Morningstar US Fund Inflation-protected bond category, Real Estate by the Morningstar US Fund Real Estate category, International stocks by the MSCI EAFE NR Index, U.S. stocks by the S&P 500 Index, U.S. bonds by the Bloomberg US Agg Bond TR Index, and Long U.S. bonds by the Bloomberg US Treasury 20+ Yr TR Index. 1. Morningstar as of 12/31/21. 20-year correlation with US BLS CPI.

Why bank loans now?

Bank loans are one of the highest income asset classes in today’s environment and are a natural consideration for investors looking for income and short duration exposure. Investors in bank loans have three potential sources of return:

1) Floating rate tied to a short-term interest rate, typically LIBOR or SOFR;

2) Credit spread determined by the issuer’s credit rating, among other factors, and

3) Price return if a loan is purchased below par value.

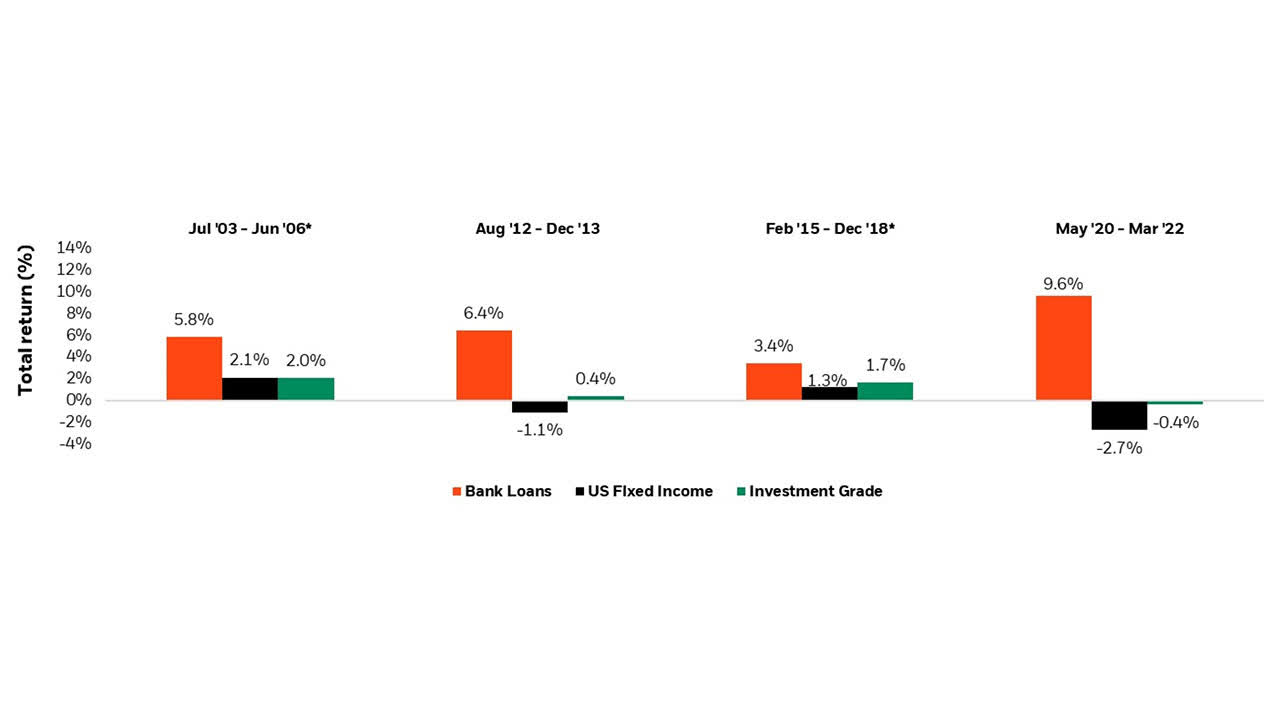

The “floating” coupon feature reduces interest rate sensitivity for bank loans which has contributed to the asset classes historical outperformance relative to “fixed” income assets in rising rate environments (Exhibit 2).

Exhibit 2: Bank Loans have outperformed traditional fixed income assets during periods of rising interest rates

Annualized Total Return in periods of rising 10-year treasury rates

The figures shown relate to past performance. Past performance is not a reliable indicator of current or future results.

Source: S&P LCD, Barclays, Bloomberg as of 3/31/22. “US Fixed Income”= BbgBarc US Aggregate Index, “Bank Loans”=S&P Leveraged Loan Index, “Investment Grade”= BbgBarc US Corporates Index. Index performance shown for illustrative purposes only. It is not impossible to invest directly in an index.*Represents periods when the Fed made explicit changes to the Fed Funds Rate (FFR).

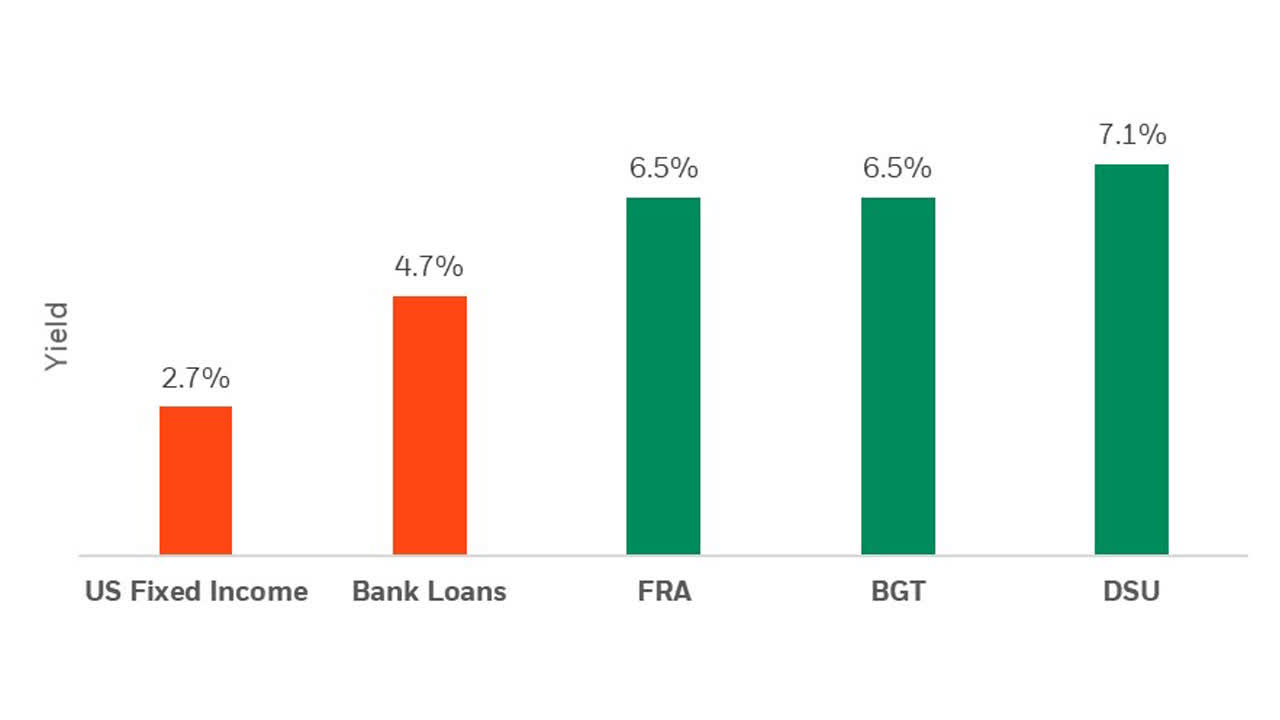

BlackRock Bank Loan CEFs invest in loans with lower credit ratings given the yield pickup may outweigh the potential risk of default. For example, defaults in bank loans are near their lowest levels in over a decade1. Additionally, issuer fundamentals are sound with company earnings improving and rating agencies accelerating credit upgrades. Further, the “closed” structure permits investment in less liquid parts of the loan market that may compensate investors for that additional risk via a higher credit spread. Finally, BlackRock Bank Loan CEFs often borrow money at lower short-term interest rates and invest that money in higher-yielding loans which may increase the income paid to holders of the fund (Exhibit 3).

Exhibit 3: Bank Loan CEFs provide competitive distribution rates

Source: Lipper and Morningstar as of 4/27/22. Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. You cannot invest directly in the index U.S. fixed income represented by the Bloomberg US Agg Bond TR Index, Bank loans by the S&P/LSTA Leveraged Loan TR Index. FRA, BGT, and DSU’s distribution rate is calculated by annualizing the latest declared distribution and dividing by the fund’s market price as of 3/31/22. In 2021, FRA’s distribution was 16.64{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} return of capital, BGT’s distribution was 15.52{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} return of capital, and DSU’s distribution was 15.09{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} return of capital. More details here: https://www.blackrock.com/us/individual/literature/tax-information/2021-taxable-closed-end-fund-distribution-breakdown.pdf

Keep an eye on discounts

Currently, BlackRock Bank Loan CEFs trade at a median discount to net asset value of -8.9{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b}. This is wider than their 1-year median of -3.9{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} but narrower than their 3-year median of -10.5{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b}. Purchasing a CEF at a discount increases an investor’s yield and can potentially lead to additional capital appreciation if discounts narrow, or trade at a premium, due to investor demand for the asset class.

Below are the premiums/discounts and distribution rates of the BlackRock Bank Loan CEFs:

Source: BlackRock as of 5/4/2022. Distribution rate is calculated by taking the latest declared distribution, annualizing it, and then dividend by the market price on the stated date. In 2021, FRA’s distribution was 16.64{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} return of capital, BGT’s distribution was 15.52{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} return of capital, and DSU’s distribution was 15.09{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} return of capital. More details here: https://www.blackrock.com/us/individual/literature/tax-information/2021-taxable-closed-end-fund-distribution-breakdown.pdf

It’s important to understand how interest rate increases flow through to bank loan investors, including BlackRock Bank Loan CEFs – in this section we’ll discuss three relevant topics, rate resets, rate floors, and borrowing costs.

Resets and Floors: The ‘floating’ component of a bank loan resets periodically and will dictate when investors realize the benefit of rising rates. Coupon rates are initially set when a bank loan is issued, comprised of a benchmark interest rate (historically LIBOR and, going forward, SOFR) plus a credit spread. Coupon payments are reset regularly (typically every 3 months) throughout a loan’s life. Thus, as a loan’s benchmark interest rate fluctuates, so too can the loan’s all-in coupon rate. However, depending on prevailing interest rate conditions, loans may be issued with “floors” against their benchmark interest rates. These floors may help insulate an issuer against near-term rising rates, but also ensure that in a period of falling-rate conditions coupon is protected for lenders. More than 80{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of loans have a LIBOR floor less than 75bps2, which implies that almost the entire bank loan market may benefit from each additional rate hike from the Fed given today’s 3-month LIBOR rate.

Borrowing costs: as discussed earlier, BlackRock Bank Loan CEFs often borrow money to earn a spread between low borrowing costs and the higher coupon paid on bank loans. The interest rate a fund pays to borrow money will fluctuate daily based on movements in short-term rates such as LIBOR whereas the coupon received on bank loan investment typically resets every 30 to 90 days. This difference may result in a short-term reduction in fund earnings. Importantly, the higher borrowing costs only impact a portion of the portfolio whereas rising rates generally benefit the entire portfolio. For example, consider a fund with $800 in assets that borrows $200, thus increasing the fund size to $1,000 (20{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} leverage). If LIBOR increases 1.00{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b}, the fund will initially pay an additional $2 in borrowing costs. When the loan resets, the fund will earn an additional $10 on its investments or an $8 spread.

© 2022 BlackRock, Inc. All rights reserved.

1. Source: S&P LCD as of 3/31/22.

2. Source: BlackRock, LCD as of 3/31/2022

Carefully consider the Trust’s investment objective, risk factors, and charges and expenses before investing. This and other information can be found in the Trust’s prospectus which may be obtained by visiting the SEC Edgar database. Read the prospectus carefully before investing.

This material is for informational purposes only and is not intended to be relied upon as research or investment or tax advice, and is not a recommendation, offer or solicitation to purchase or sell any securities or to adopt any investment strategy, nor shall any securities be offered or sold to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction.

There is no assurance that a fund will achieve its investment objective. Investing in a fund involves numerous risks, including investment risks and the possible loss of principal amount invested. The funds are not complete investment programs and you may lose money investing in a fund. An investment in a fund may not be appropriate for all investors.

Performance results reflect past performance and are no guarantee of future results. Current performance may be lower or higher than the performance data quoted. All returns assume reinvestment of all dividends and/or distributions at the price of the fund on the ex-dividend date. The dividend yield, market value and net asset value of a fund’s shares will fluctuate with market conditions. Closed-end funds may trade at a premium to NAV but often trade at a discount.

S&P Leveraged Loan All Index – an unmanaged index comprised of loans that meet the following criteria: at least $50mn in size contract size, minimum initial spread of LIBOR + 125, and a minimum term of at least one year at inception.

The amounts and sources of fund distributions reported in any notices to shareholders are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon a fund’s investment experience during the remainder of its fiscal year and may be subject to change based on tax regulations. A fund will send a Form 1099-DIV for the calendar year that will tell shareholders how to report these distributions for federal income tax purposes. Some funds make distributions of ordinary income and capital gains at calendar year end. Those distributions temporarily cause extraordinarily high yields. There is no assurance that a fund will repeat that yield in the future. Subsequent monthly distributions that do not include ordinary income or capital gains in the form of dividends will likely be lower.

Some investors may be subject to the alternative minimum tax (AMT).

The Funds are actively managed and their characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Principal of mortgage- or asset-backed securities normally may be prepaid at any time, reducing the yield and market value of those securities. Obligations of U.S. government agencies are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US government. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher rated securities. Investments in emerging markets may be considered speculative and are more likely to experience hyperinflation and currency devaluations, which adversely affect returns. In addition, many emerging securities markets have lower trading volumes and less liquidity. A Fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. Refer to a Fund’s prospectus for more information.

55 E 52nd St, New York, NY 10055.

©2022 BlackRock, Inc. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USWAH0522U/S-2117838-5/5

This post originally appeared on the iShares Market Insights.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.