Matthew McInerny

Timothy Rabe

CIO: We noticed history issuance of floating-level financial institution loans in the first quarter of 2021, and there is nevertheless a large calendar of offerings ahead. What’s driving the hunger for this kind of personal debt?

Matthew McInerny: We believe that we’re at an appealing entry level for this asset course the two simply because it features yield in a minimal-yield setting and mainly because there is not a good deal of distress in the industry right now. In addition, financial institution bank loan functionality traditionally correlates carefully with inflation, which has been trending larger, and larger inflation tends to direct to climbing interest rates that raise yields on floating-charge loans. At the very same time, the Federal Reserve has indicated it could start out tapering its quick-dollars insurance policies prior to 12 months-conclusion. If that takes place it would likely drive shorter-phrase prices increased, too. We would then be expecting the ordinary spread as opposed to LIBOR [the benchmark interest rate at which major global banks lend to one another] in the financial loan market place to widen a little bit from the 417 foundation factors [bps] that prevailed in early September.

Timothy Rabe: We are in sort of a Goldilocks era proper now. You are seeing upgrades outpace downgrades and just about everything in the bank loan marketplace is carrying out quite very well. Even if fixed-money marketplaces weaken, loans are at the prime of the cash structure and backed by collateral, so recoveries tend to be better than they are for unsecured bonds. Nonetheless, we believe recoveries will keep on to drop as there are now a expanding quantity of borrowers who problem only in the mortgage current market rather than in both of those the personal loan and superior-generate markets.

CIO: How interesting is the new offer on the way, and what is driving all the issuance?

McInerny: There is about $60 billion of provide we can see. A ton of it will finance company M&A [merger and acquisition] exercise, which is our most well-liked kind of financing for the reason that there is no sponsor involved, there are far better credit history arrangement files, and there are typically higher good quality companies associated, usually with BB credit ratings.

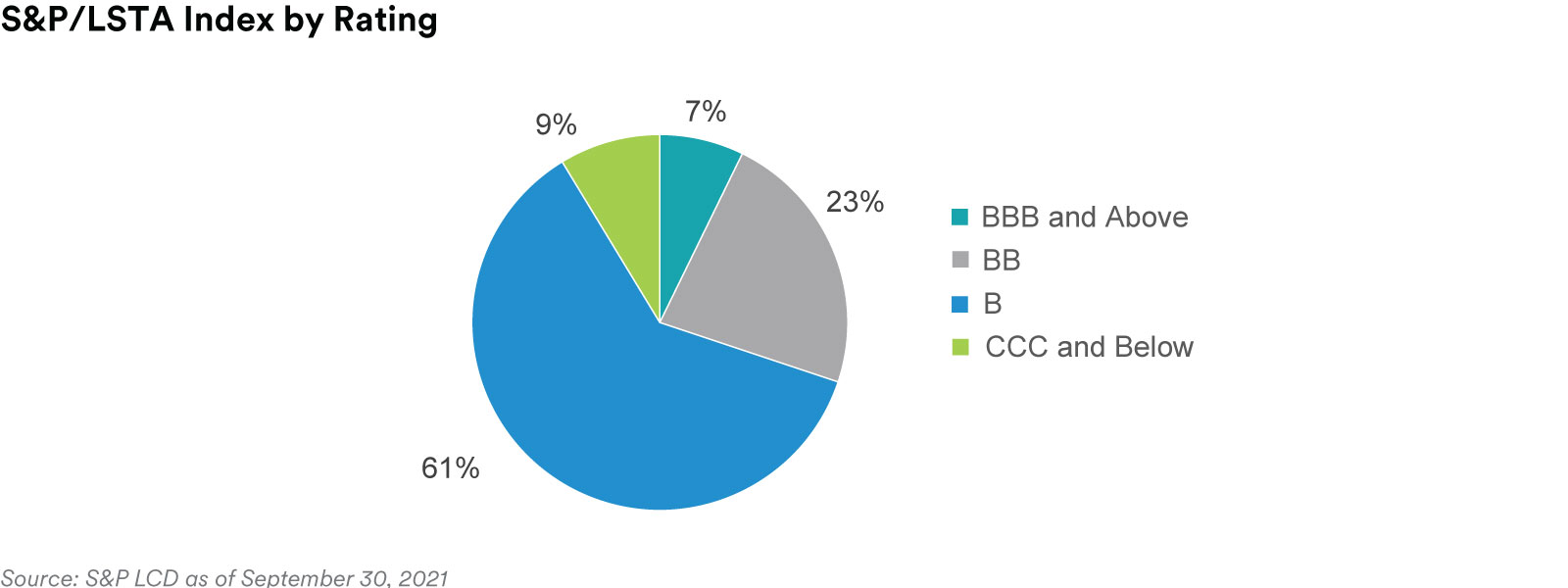

CIO: What does the market seem like outside the BB sector?

McInerny: The market has 4 principal categories. The expenditure-quality [IG] BBB sector represented about 7{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of the industry as of September 30. We believe that that IG loan yields are attractive vs . comparable maturity US IG bonds. A single notch down on the credit score scale is the BB sector, which is about 23{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of the personal loan industry. Up coming are B-rated financial loans, representing about 61{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of the industry, up from 43{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} five a long time back. These loans are well-known funding vehicles for leveraged buyouts. The reason industry share for this sector has risen so substantially is simply because collateralized bank loan obligations, or CLOs, have become a much even larger element of the market place and CLO structures involve, between other factors, loans with an typical score of B. The last group is CCC financial loans and unrated loans, which incorporates defaulted loans, symbolizing about 9{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of the industry.

CIO: Exactly where are the most effective values to be located currently?

McInerny: We are locating pockets of chance in BB loans, as perfectly as inside the single-B place.

CIO: How is the progress of CLOs impacting the prospect for other investors?

Rabe: The key for a CLO is finding a diversified team of loans that suits its structure. Over and above scores, it seems to be at variables this sort of as restoration scores, field, and market place price—things that don’t usually have to do with the fundamental credit rating. That creates opportunities for us to look at financial loans that don’t work for a CLO, such as financial loans trading under 80{797b2db22838fb4c5c6528cb4bf0d5060811ff68c73c9b00453f5f3f4ad9306b} of par in occasions of market stress. Those people financial loans could stand for a good risk-reward opportunity for us.

CIO: Talking of chance, what would you caution an trader to be conscious of when moving into this market?

Rabe: The major misconception about lender financial loans is a belief in their inherent security just due to the fact they are secured. Common wisdom suggests financial loans give you most of the upside of the large-generate market with much fewer draw back. But about the earlier decade, a developing proportion of the current market has appear to be represented by debtors who are issuing financial debt only in the mortgage industry. In that circumstance, they’re not considerably distinctive than a significant-generate issuer. Indeed, their financial loans are secured by property, but there is generally no subordinated credit card debt in the borrower’s capital structure—no cushion to eat as a result of right before obtaining to the loans. On top rated of that, loans are callable at any time at 100 cents on the dollar, so your upside is essentially zero if you acquire near par. People at times get lulled to rest with financial loans, but when all chance markets do inadequately, loans participate nearly as significantly as large-generate does. Also, the protections on loans normally are not as excellent as they utilised to be due to the fact so a lot of loans issued nowadays are “covenant lite,” this means they have less restrictions on the borrower and fewer protections for the financial institution.

CIO: Should really covenant-lite financial loans be avoided then?

McInerny: Traders really should understand their traits, but we experience it is neither good nor simple to avoid them. Even when they don’t have upkeep covenants, financial loan credit rating agreements are usually nevertheless of bigger top quality than bond indentures.

CIO: How is MIM positioning its mortgage portfolios in this ecosystem?

McInerny: In general, we believe that you keep out of problems in the financial loan industry by finding the right credits. In a industry like this, it is extra important not to extend to get one thing in which you are not adequately staying paid out for the further chance. Suitable now, we’re skewing towards large credit-excellent financial loans simply because you want the skill, when the market place does right, to go decreased in credit rating high quality and obtain securities that have come to be stressed or distressed.

CIO: How challenging or quick is it to uncover the right credits?

Rabe: In contrast to with public securities, debtors do not commonly publish a whole lot about their financials once their loans are in the market place. We believe that that offers an edge in the secondary marketplace to anyone like us, who vetted all those financial loans right before they have been designed and possibly even participated in them. It provides us info that may well be valuable later on should the borrower, or even an whole sector or the entire marketplace, have difficulties.

CIO: What distinguishes your solution to study?

McInerny: We have pretty expert portfolio professionals backed by a deep investigation team of 35 men and women. Our group leaders on normal have extra than 20 several years of practical experience, which includes major sector expertise, which we truly feel is key as they’ve invested in people sectors about distinctive financial cycles. We feel that can enable gives us an gain when the market place sells off there are specific credits we suspect are likely to get oversold, that we’re going to want to increase to our portfolio. An additional characteristic at MIM is that we have a investigate crew in London, which will help with investing in European cross-border issuance.

CIO: How else can potent research incorporate value?

McInerny: Our depth and expertise enables us to be energetic in the center sector, which can help us include price for our customers. For example, we experienced a center-current market issuer appear to market place a short while ago with a personal loan we ended up closely associated in negotiating the credit score agreement and inserting meaningful improvements to protect buyers. All those sorts of possibilities can probably increase alpha to a portfolio, but you need to have an expert and deep study staff to dig by means of those credits and come across the types that make sense. Some CLOs prohibit center marketplace loans in their portfolios.

CIO: Do you see any rewards for traders to participating in the financial institution bank loan marketplace outside the house of structured products like CLOs?

Rabe: Even though the current market has been on an even keel, we assume even extra eye-catching options the up coming time it goes down. When it does, we’re going to have the capability and assets to set money to perform. When you own a remarkably diversified financial loan portfolio with a large amount of distinctive issuers, the way a large amount of CLOs do, you are heading to have a lot of distressed issues to operate by means of in a downturn, which can cease you from allocating cash on the other facet. We request to steer clear of that by holding a portfolio that is fairly concentrated with the aims of averting credit history threat and possessing the time and ability to put capital to work at reduced concentrations.

CIO: How is this mirrored in portfolio effectiveness over the prolonged haul?

Rabe: When a greater mortgage portfolio might are inclined to monitor the financial loan index quite carefully, our a lot more concentrated portfolio seeks to push effectiveness with strong safety choice. An investor may well want to talk to no matter whether they are basically seeking for blanket exposure to the loan sector or alpha within that exposure. We’re attempting to deliver alpha inside the exposure.