One day last September, while trying to pay for groceries, Leslie Alvarez got the shock of her life. All the money in her bank account had disappeared.

The Houston single mother called her bank. An employee told Alvarez that her accounts had been placed on a legal hold. A person she did not know had been authorized to remove money from her accounts.

“I had to tell my kids they had to wait awhile so I could go make money to get what they needed,” she said.

Alvarez was forced to pay up on a $1,500 cash loan as part of a debt judgment issued against her in a Harris County civil court.

Texas doesn’t allow people’s wages to be garnished to pay off debts unless it is to collect child support. By law, however, courts can designate special officers, known as turnover receivers, to force payments by freezing or seizing bank accounts. The legal process became popular in Harris County but has been used all over the state more commonly in recent years, officials say.

“This is the only real way a debt collector can hurt you,” said Craig Noack, a creditor’s attorney in San Antonio who also serves as a court-appointed receiver in Texas.

At issue, though, is whether courts have adequate oversight to ensure a fair process.

Each year, tens of thousands of Texans are subject to a bank seizure as a result of a default judgment that was declared against them because they didn’t show up in court to fight a lawsuit over a debt.

But here’s the dilemma: Most debtors don’t know that they can have their bank accounts cleaned when a debt collector wins a default judgment against them unless they claim exemptions for certain sources of funds, such as child support, Social Security, unemployment benefits and retirement funds. Alvarez had child support payments in her accounts when they were seized.

Just this month, the Supreme Court of Texas took its first steps to establish parameters that would ensure that debtors are informed of their rights to claim exemptions. Under new rules, which took effect May 1, debt collectors must provide at least 17 days for debtors to inform courts that they have funds or property that is exempt from seizure.

“The purpose of these rules and forms is to try to help even out a little bit the playing field so that the debtors get more information,” Texas Supreme Court Chief Justice Nathan Hecht said.

The notifications come at a time when debt collection lawsuits statewide have skyrocketed. Hundreds of thousands of Texans are being sued by debt collectors over unpaid credit cards, medical bills, student loans and other debt, according to a Houston Chronicle examination of court records, observation of legal proceedings and a review of data on court dispositions.

SECOND IN A THREE-PART SERIES

A Houston Chronicle investigation has found that an explosion of debt collection lawsuits filed in Texas is raising concerns that overwhelmed civil courts can’t adequately review each lawsuit and deliver justice fairly.

APRIL 28

Debt collection lawsuits filed in Texas have soared by 73 percent over the last decade.

MAY 5

A growing number of Texans could unknowingly be subject to a bank freeze or accounts seizure.

MAY 9

A North Texas couple fights back and sues their credit card company, a debt collector and two credit bureaus.

For the first time last year, the 374,000 debt lawsuits filed in the Lone Star State made up nearly half of all civil cases in Texas, which include traffic tickets, landlord evictions and small claims such as disputes between neighbors, according to data from the Texas Office of the Court Administration.

Meanwhile, default judgments — the window of opportunity for the seizures — nearly exceeded 90,000 last year statewide.

In the Houston region and other large Texas counties, default judgments rose by 86 percent between 2012 and last year, data show.

“As long as people don’t respond, debt collectors can get a default judgment,” said Ann Baddour, director of the fair financial services project at Texas Appleseed, a consumer advocacy group in Austin. “There’s just this motivation to move forward and sue.”

Even the Texas Creditors Bar Association, a statewide organization of attorneys that engages in debt collections, says it wants to make sure debt collectors don’t take money that is protected by law.

They support the notifications, said Noack, who represented the Texas Creditors Bar Association in discussions before the Supreme Court Advisory Committee about the new rules.

“You’re not going to find a creditor’s attorney out there who wants to take somebody’s Social Security,” he said.

Yet, among the many concerns consumer advocates say still must be addressed is the lack of oversight in Texas courts regarding the appointment of the court officers or turnover receivers.

Texas courts have no way to prevent abuses — or even mistakes — because judges are not required to track their appointments or keep periodic reports on the status of seizures, Houston consumer attorney Benjamin Sanchez said.

“You have these receivers who are doing things but not necessarily reporting back to the court,” Sanchez said.

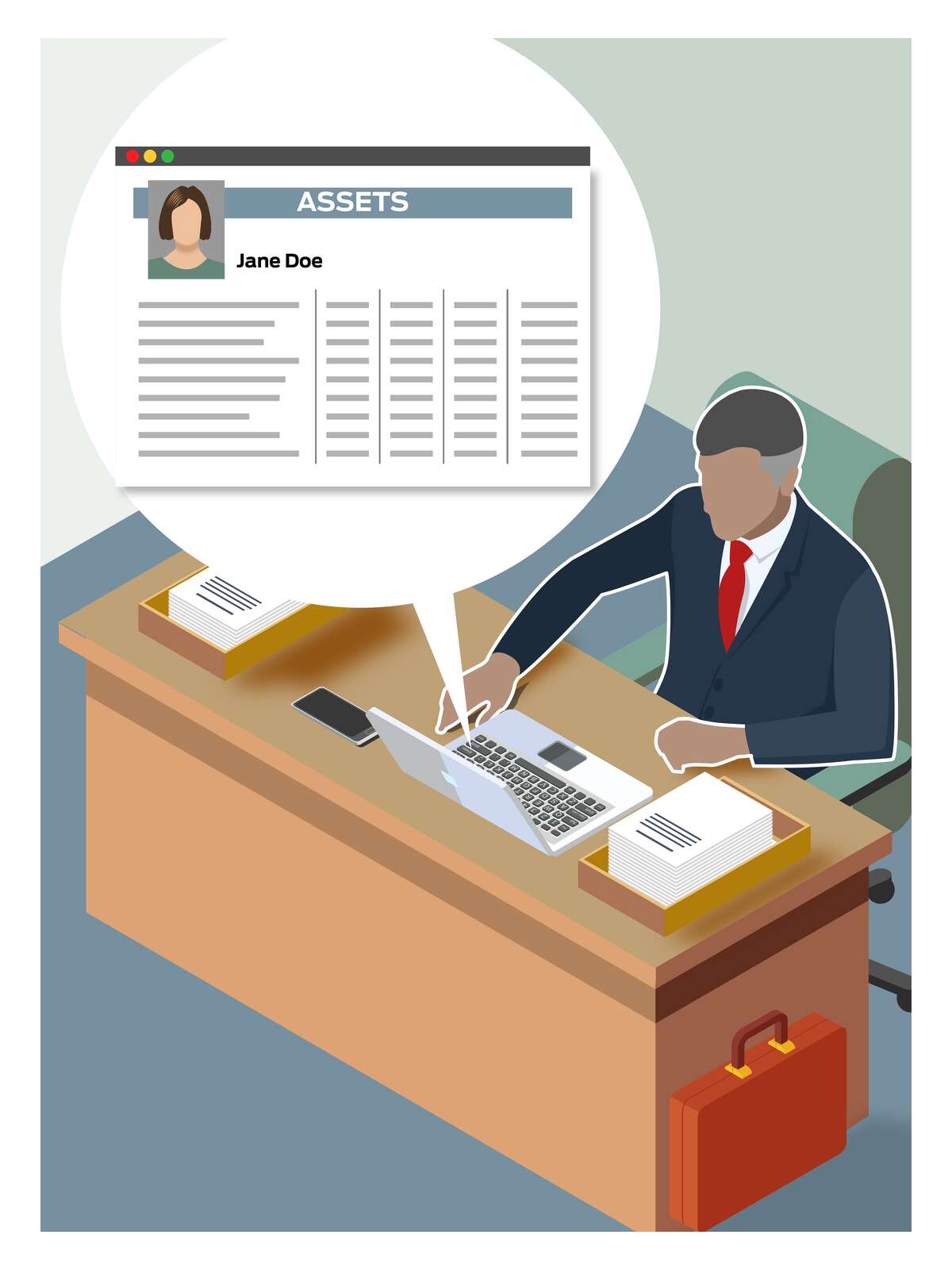

How a debt collector can seize your bank accounts without you knowing it.

Jane Doe has a debt judgment against her — meaning that a court

has ordered her to pay a debt she owes.

Her creditor now can ask a court to appoint a special officer,

known as a turnover receiver, to collect the debt. The creditor

must file an application with the court for a turnover order and

the appointment of a receiver.

Some courts will demand that the creditor provide notice to Doe of

the requested appointment of a turnover receiver, but it is not

required. Under a Texas Supreme Court rule that went into effect

May 1, receivers must notify Doe of her exemption rights. Under

Texas law, certain assets and sources of funds, such as government

and retirement benefits and child support, are exempt from

seizure.

The turnover receiver will seek out different sources of

information to learn about Doe’s non-exempt assets. Often, the

receiver will utilize financial resources, such as a credit

report, to identify Doe’s bank.

The turnover receiver will send a letter to the bank notifying it

that the receiver has been appointed by a court to freeze or

remove money from Doe’s bank accounts.

The turnover receiver must provide a copy of the court order

appointing him or her as the turnover receiver. The bank will

ordinarily freeze or hand over funds to the receiver, but banks

are obligated to protect two months’ worth of federal benefits,

like Social Security, and typically will not hand over those

funds.

The turnover receiver will evaluate whether Doe can afford to pay

the debt. If Doe has plenty of money in the bank to cover it, the

receiver will be less inclined to agree to a payment plan.

There is an even greater potential for harm in a state with the highest percentage of its population with delinquent credit, consumer advocates said. In December 2020, 41 percent of Texans had defaulted on accounts sent to collections, according to the Urban Institute’s Debt in America report.

After they’ve frozen someone’s bank account, a debt collector can use leverage to coerce a settlement from a debtor, said April Kuehnhoff, staff attorney at the National Consumer Law Center in Boston.

“This is absolutely an extremely aggressive method of debt collection,” said Kuehnhoff, who studies debt collection practices across the U.S. “I am not aware of any other state that uses a turnover receiver for collection of consumer debts or judgments.”

In Houston, Sanchez said he’s spoken with debtors who had more money taken from their bank accounts than was owed because they had missed a few months of a settlement plan. He said the money was removed without their knowledge.

Debtors can easily fall into a financial crisis if there is no money left over after a seizure to pay for rent, child care and other basic living expenses. Without money for a car payment, debtors can have trouble getting to work, causing an even deeper spiral.

The consequences can be devastating, said Rogelio “Roger” Lopez, Precinct 4 judge in Bexar County.

“Just because you have a default judgment doesn’t mean you get to destroy somebody’s life,” Lopez said.

Alvarez, the Houston single mom, didn’t know that state law protected child support payments from the grasp of a debt collector, said Richard Tomlinson, director of litigation at Lone Star Legal Aid of Houston, who served as her attorney.

Tomlinson filed a motion in Harris County Justice of the Peace Court Precinct 1, Place 2, on her behalf in October to get the money back, but there was over a four-month delay.

The court, struggling to clear out cases in the middle of a pandemic, couldn’t find a date available for a hearing.

She finally got a hearing in January. At the court proceeding, Tomlinson argued that the seizure had been unlawful because the turnover receiver took Alvarez’s child support funds. He had to provide the court with documents that showed the funds had been placed in a bank account that contained child support payments.

Alvarez received her refund check on Feb. 9.

“It made me feel like a bad mom when they froze my accounts and took their (her children’s) money because they had nothing to do with this,” Alvarez said.

Defendants listen as Tarrant County Judge Ralph Swearingin Jr. explains the voluntary mediation program for defendants and debt collectors appearing in his Fort Worth courtroom.

Mark Mulligan, Staff photographer/Houston Chronicle

Eluding exemptions

Over a century ago, the state’s founders aimed to protect Texans from financial calamity. So, they conjured up — as part of the state’s Constitution of 1876 — a lengthy list of exemptions that debt collectors could not take. They included people’s homesteads, livestock, up to two firearms, wedding rings, heirlooms and religious books.

Back then, it was illegal for a debt collector to ask a Texan to turn over cash or assets. But everything changed — though the list of exemptions did not — when banks were established and they later introduced direct deposit.

By law, wages deposited in a bank account could be subject to a garnishment. But the process soon fell out of favor with creditors because it required them to file a separate lawsuit, known as a garnishment proceeding, against banks. They also had to pay additional filing fees and cover charges for bank attorneys.

“You may not get enough money to pay the bank’s lawyer, and then they dismiss you and you’ve lost the money and labor you spent on the case,” said Tomlinson, who is a former assistant attorney general in the consumer protection division of the Texas Office of the Attorney General. “Nobody wants to go back and have dry holes.”

Over a decade ago, a small group of Harris County attorneys decided an alternative was necessary. They tapped a state law that allowed special officers to be designated by courts to enforce judgments in debt collection cases.

“For years, it was just kind of laying in the weeds and nobody used it,” said Paige Hoyt, supervising attorney at Legal Aid of NorthWest Texas in Fort Worth.

There was no filing fee required, and the creditor could still be paid the entire amount of the money owed on the judgment.

“It’s just one more motion, you point your button, your form comes out,” said Riecke Baumann, a Houston creditor’s attorney who serves as a court-appointed receiver in Texas. “You have a hearing. And then, as the plaintiff’s attorney, you can pretty much close your file.”

As word got out, creditor attorneys lobbied the Legislature to affirm that turnover receivers could be appointed in justice of the peace courts, where it is cheaper to file and faster to win judgments. As a result, the number of debt lawsuits jumped by nearly 150 percent from 2015 to 2020 in JP courts. Of the hundreds of thousands of debt collection lawsuits filed last year, 80 percent were in JP courts.

Creditors also argued it was too expensive to make a request for a bank garnishment in order to satisfy a debt judgment. It was already a challenge to compel people to show up for court before judgments were signed off by judges. Many people didn’t respond to letters from creditors’ attorneys. They ignored court summons to appear at discovery hearings to force them to provide payroll and bank information, they said.

Most debtors want to resolve the matter and get on a payment plan, Noack said. A turnover receiver can be very effective to try to work out a deal, he said.

Once a bank account is frozen, Noack said he attempts to settle with the debtor. When the two parties can reach an agreement, Noack can unfreeze bank accounts within 48 hours. It’s unfortunate, but there is no better way in Texas to get debtors’ attention, he said.

“In Texas, your job as a creditor’s attorney is that you have to have (debtors) arrive at that ‘Come to Jesus moment,’ one way or another,” he said. “You can’t just ignore this forever. That’s the whole point.”

Most professional collectors don’t use tactics that will impoverish people, Baumann said. They benefit more from allowing debtors to keep cars so they can go to work and afford to pay back obligations. They don’t wipe out bank accounts.

That’s one reason the Texas Creditor’s Bar favors sending notices to debtors of their exemption rights, Baumann said.

“It’s good public policy,” he said.

This is a carousel. Use Next and Previous buttons to navigate

Agonizing discussions

As impartial officers, judges say they must be fair. Their role prohibits them from providing legal advice or doubling as the debtor’s attorney.

They say an order for payment on a debt judgment gives them little flexibility. They may step in to raise an objection, but those instances are not common.

In a late February Zoom session, Judge Ralph Swearingin Jr., justice of the peace for Precinct 1 in Tarrant County, spelled out for 34 defendants who were due in court that morning what could happen if he granted requests for the appointment of turnover receivers.

“I want to explain to you what in the world is going on,” he said. “You, the debtor, was sued by a debt collector. That same debt collector won a judgment against you for the debt he said you owed. By law, the collector can ask the court for assistance to collect the debt.”

Your favorite boat could get swiped, he warned. Or even your prized Jet Skis.

What could happen?

“You may get a call from them,” Swearingin said. “‘I’m down at your bank. I’d like you to come down and talk to me before I take this money out of your bank account.’”

Similar agonizing discussions are going on all over the state, virtually and in-person.

That morning in Swearingin’s court, a Fort Worth woman who faced a judgment for $1,300 was among the first to pop up. She told the judge that she had already reached an agreement to pay the money she owed. Would the judge advise her on how she could make sure that her credit report showed that she had paid in full?

His comment: She’d have to resolve the matter herself.

He then denied the request for an appointment of a turnover receiver in her case.

Next, another Fort Worth woman told him she wasn’t aware that she had a $6,700 judgment against her. Court records showed an attorney had filed a response to the court on her behalf in December 2020. But she said she had been battling COVID while trying to fax information to the attorney.

“But I just found out two days ago that they hadn’t done anything,” she said.

All he could do, Swearingin told her, was to place her in a breakout room, where she could join other debtors trying to cut deals with receivers who had been appointed in their case to collect on their debts.

Court records suggest she worked out a deal because the creditor that same day withdrew the application for a receiver.

A few weeks before that hearing, Sharolyn Wood, a former Harris County district court judge who was filling in for David Patronella, Harris County Justice Court Precinct 1, Place 2, had to explain to another debtor that she was required by law to grant the request for a receiver.

On Zoom, the Houston man said he wanted to challenge the debt judgment against him.

“I think he really scammed me,” he said, referring to the debt collector. “It’s really sad this has happened.”

But he hadn’t filed any paperwork, the judge said. Wood had to rule based on the information in front of her and grant the receiver request.

“I have to honor the judgment and follow the law with regard to that judgment,” the judge told him.

The Tarrant County courthouse in Fort Worth has seen a growing number of debt collection lawsuits filed against consumers.

Mark Mulligan, Houston Chronicle / Staff photographer

‘Life events happen’

Some consumer advocates say they don’t object to bank seizures when they are applied to entities that may be trying to hide large assets from creditors or one another. The process has been effective in prying loose assets in a divorce when one party is withholding information from another.

The concern, however, is with debt collectors who zero in on wage earners who have limited disposable income to support basic needs.

“These are people who are struggling to get by who suddenly find themselves at the mercy of this very aggressive debt collection procedure,” said Kuehnhoff, the staff attorney at the National Consumer Law Center.

Amy Beth Clark-Downing, a consumer attorney at Texas RioGrande Legal Aid in Austin, said she has clients who have teetered on homelessness after money has been taken from their bank accounts.

In some of those cases, clients have not been aware that a debtor has won a judgment against them.

Alvarez, the Houston mother who had her child support seized, had moved when the process server arrived to present her the papers on the underlying debt claim, said Tomlinson, her attorney. It’s unclear whether another person — maybe a relative — was handed the papers, he said.

Debtors with lower incomes tend to be more transient as they move from place to place looking for work and stability, Clark-Downing said. That means sometimes they can’t be located by a process server.

Other times, they may be living with a family member or friend, who steals their identity to apply for cash loans, said Clark-Downing, who is also the manager of the consumer protection team at the Legal Aid office.

In those cases, Clark-Downing said she presses debt collectors to show documented proof that her client was the one who took out the loan.

During the pandemic, she spent months trying to get hearings for debtors to get their money back or to try to reach settlements.

Early this year, Clark-Downing filed a petition urging a Bexar County justice of the peace court to set aside the debt judgment of a 58-year-old San Antonio man who had more than $1,000 removed from his bank account on a debt he said he didn’t owe. But the man’s case sat for months while the court halted its normal activities during the pandemic and she tried to negotiate with the debt collector. He almost faced eviction and struggled to pay child care for a grandson, Clark-Downing said. She advised him to file for bankruptcy to get his affairs in order.

Three months after the pandemic started, Deanna Bleacher received a letter from her bank saying $1,900 had been removed from her checking and savings account, court records showed. The Webster woman learned that a turnover receiver had been appointed to recover a default in her name on a loan with a principal amount of $1,300.

Weeks later, as she struggled to make ends meet, she found a Legal Aid attorney in Houston who helped her recoup at least a portion of the funds, which included unemployment compensation funds that are exempt by law.

Megan Daic, a consumer attorney in Houston, said similar stories are common. Since the pandemic, many more modest- to middle-income consumers have called her for help to untangle a financial crisis after a turnover receiver has been appointed to their case.

Compared to the indigent, these Texas wage earners tend to have more access to credit — and can encounter hardship when they face job loss, illness and other setbacks.

“These life events happen,” Daic said. “And that’s on top of health and medical issues, divorce. That’s usually what seems to happen, people just end up in this tough spot.”

Sanchez, the Houston consumer attorney who volunteers at a local legal clinic, said he has seen the sharpest rise in requests for legal assistance from people who are middle-income wage earners. They are not poor enough to qualify for legal assistance, yet, unlike higher wage earners, can’t afford attorneys on their own, he said.

National surveys have found that consumers with family incomes between roughly $38,000 and $55,000 were most likely to report being contacted by a debt collector while those with incomes below the federal poverty level were the second-most likely to be contacted.

At times, a delicate situation will teeter on the point of no return before a judge can untangle it, said Jo Ann Delgado, justice of the peace for Precinct 2, Place 1 in Harris County.

Not too long ago, a debt collector in Delgado’s court seized the bank account of a mother who paid her daughter’s college tuition with child support.

“She wasn’t going to be able to finish her semester because her mother’s bank account was garnished,” Delgado said. “I had them reverse it and put that money back into her mother’s bank account.”

Megan Daic, a consumer attorney shown inside her Houston office, said many more modest- to middle-income consumers have called her over the last two years for advice on debt collection cases.

Godofredo A. Vásquez, Houston Chronicle / Staff photographer

Mounting debt

This spring, the Consumer Financial Protection Bureau reported that credit card companies were expected to hike fees and penalties due to inflation and other factors. In 2020, fees topped $12 billion. The New York Federal Reserve Bank reported the largest quarterly increase in 22 years of credit card balances in the fourth quarter of 2021 — suggesting more people will fall behind on payments and be subject to lawsuits.

In Texas, judges expect to see an increase in the number of people who will appear at hearings to keep debt collectors at bay.

Judges said they will have to squeeze more time into their dockets to review information with debtors about their exemptions. Debtors who claim exemptions will have to submit documents to prove they are valid.

“We want to make sure the language is crystal-clear and everyone is able to understand what is being said and what is required,” said Sergio De Leon, justice of the peace for Precinct 5 in Tarrant County.

Creditors also will have to submit more paperwork. The rule requires that the officers who are appointed as turnover receivers mail debtors the notifications of their right to claim exemptions, said Noack, the San Antonio creditor’s attorney who also serves as a court-appointed receiver in Texas courts.

Hecht, the chief justice for the Texas Supreme Court, said the justices spent many hours weighing the new rules requiring debtors to be informed of their exemptions. The goal is to help balance the interests of all parties.

“The court system needs to make sure that these processes are fair, understandable, accessible, and that’s why we’re trying to do this,” Hecht said.